Wouldn’t it be good should you have a gold-mine you to you can utilize when you needed currency? If you have had your property for a while, you’re sitting when you look at the a gold-mine and never actually realize it. Making use of family collateral can be a great way to accessibility money in the interest rates which can be a lot better than simply playing cards.

The basics of household security credit

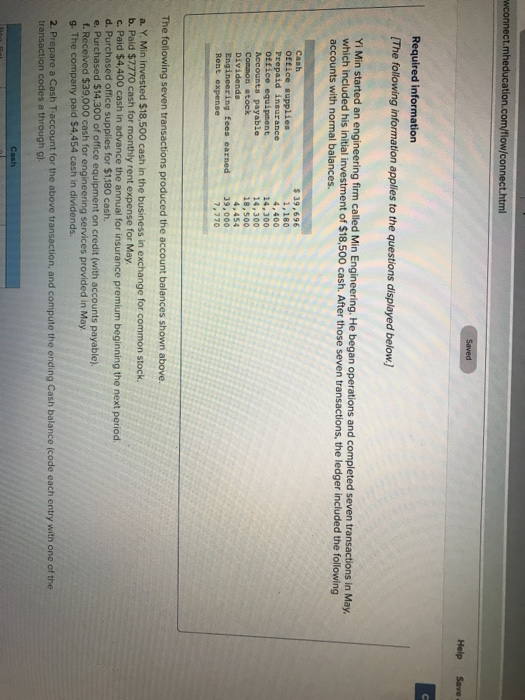

New equity of your property is what it’s currently worthy of (ount you borrowed from on the financial, which is sometimes called their first mortgage. Equity is built if worth of your home grows and as you ount you owe by creating their home loan repayments. Just how far security are you experiencing?

Can you imagine the marketplace worth of you reside $100,000, while owe $55,000 on your first-mortgage. Congratulations! You have got guarantee of your house value $45,000.

So do which means that the entire $forty five,000 is obtainable so you can borrow thanks to a property collateral mortgage or personal line of credit? Perhaps not, since most loan providers allow you to acquire doing 85% so you’re able to ninety% of your current value of your property. Getting a loan provider who has an enthusiastic 85% restrict, would certainly be able to use $31,000 on top of your residence financing. For your requirements mathematics lovers, here’s the algorithm: ($100,000 x 85%) minus $55,000.

2 kinds of fund and some common has actually

There are two an easy way to borrow on new security on the house. Property collateral financing and you may a property collateral credit line (HELOC). Precisely what do he’s in keeping?

The fresh new recognition processes for both types of domestic equity borrowing from the bank is actually comparable. The financial institution will appear at your credit score and you may full obligations-to-money proportion to be sure you are not borrowing from the bank more you are able. You are going to need to fill out paperwork, and the lender will likely get an assessment of your the home of make sure the market value site web is correct. And will also be expected to spend fees to apply for and you may procedure the mortgage.

Whenever property equity loan or HELOC is approved it gets an effective 2nd mortgage plus home is bound as equity. It indicates for people who end while making repayments, the financial institution is also foreclose at your residence.

Interest you only pay towards property security financing otherwise HELOC is also getting tax deductible for folks who itemize deductions as well as the money you acquire is employed to order, make or improve home that you apply given that security for the loan.

- After you receive money throughout the loan

- How costs is actually organized

- How interest levels are determined

Distinction #1: Once you get money.

That have a house collateral financing, you will get money initial. If you’d like to acquire $25,000 to fix your domestic, such as for example, the lending company usually material fee to the complete $25,000 if domestic collateral financing try issued.

An effective HELOC was a prescription amount that the lender usually assist you borrow against brand new equity in your home. If you aren’t sure what kind of cash you want or whenever, you can make use of inspections or a repayment credit that will draw money from offered line of credit financing.

Difference #2: Exactly how costs are organized.

Repayments into the a property equity financing are like your first home loan. You’re going to be considering a routine from monthly appeal and prominent costs to make in line with the label of one’s financing. Really home guarantee lines are set to have an expression between 5 and you can 2 decades.

HELOC payments are going to be organized a few suggests. The original enables you to generate attention-just payments during a-flat time for you to draw or borrow cash on the line regarding borrowing. Next demands dominant and you may appeal payments within the mark period. Both in of them products, you’ll be expected to generate attention and you may prominent repayments to spend from the line of credit adopting the mark months ends up.

Differences #3: Just how rates of interest are determined.

Household guarantee loans typically have a predetermined interest rate that will not change-over the definition of of one’s mortgage. Such pricing usually are a while more than adjustable-rate financing.

Very HELOC funds provides an adjustable interest that is modified considering alterations in common monetary benchple. With many HELOC funds, you could potentially convert the speed of varying so you can repaired.

So what is the best option?

Going for anywhere between a fixed rates, place count family equity loan and you will a variable rates, unlock personal line of credit most relies on your role.

If you want to obtain a predetermined matter and do not look for the necessity to acquire again for some time, a property equity financing offers a flat plan to blow straight back the mortgage.

But if concurrently, you’ve got a consistent need use smaller amounts and you will spend those individuals right back rapidly, the flexibleness away from an excellent HELOC would-be greatest.

Either way, tapping into the fresh new security in your home would be a way to money renovations, pay back an enthusiastic combine higher attention personal credit card debt, or give you reassurance knowing you can access dollars at the sensible cost for emergencies.